13 Data Center Growth Projections That Will Shape 2026-2030.

Data centers will require a $6.7 trillion investment by 2030 to match the growing compute power needs. This represents the biggest infrastructure investment cycle in modern history.

Data centers will require a $6.7 trillion investment by 2030 to match the growing compute power needs. This represents the biggest infrastructure investment cycle in modern history.

The global need for data center capacity might triple by 2030. AI workloads will make up about 70% of this expansion. Goldman Sachs predicts power consumption in data centers will rise by 165% from 2023 to 2030. The infrastructure market will likely exceed $1 trillion in yearly spending by 2030.

Organizations throughout the compute power value chain must invest $5.2 trillion in AI-ready data centers. New data center capacity of nearly 100GW will become available between now and 2030. This addition will double the world’s current capacity. AI could handle half of all workloads by 2030. This shift will change how we design, construct and manage these vital facilities.

Data center investments will reach $3 trillion through 2030. Companies must understand these growth patterns to navigate this evolving digital world. The infrastructure’s occupancy rate could climb from 85% in 2023 to over 95% by late 2026. These changes bring new challenges and possibilities that will influence the industry’s future.

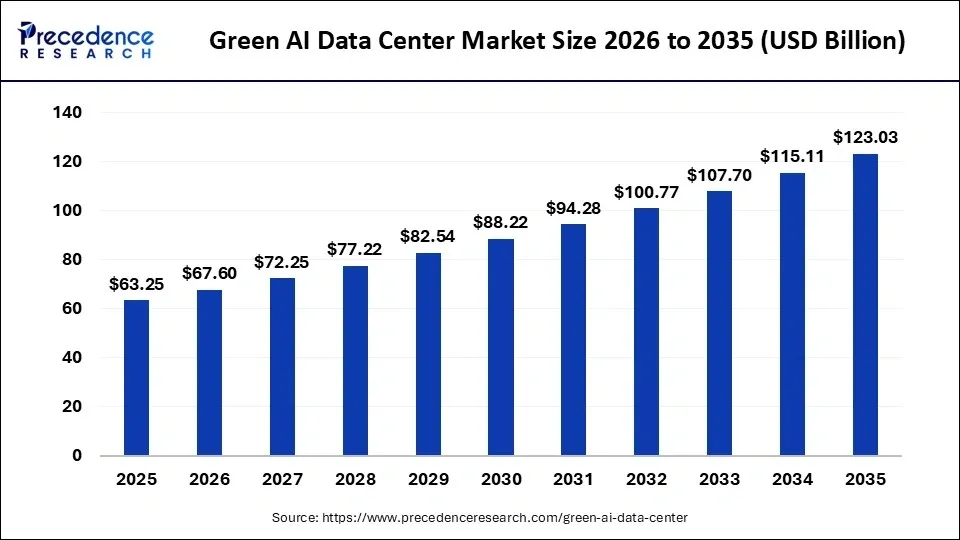

AI as the Primary Driver of Data Center Growth

Image Source: Precedence Research

AI models need innovative technology that has turned data centers into some of the world’s most important infrastructure. Tech companies are building next-generation facilities from Texas to Shanghai. These facilities house specialized graphics processing units and need high-voltage power connections to run.

AI-driven data center demand trends

US spending on data center construction has tripled in the last three years. New facilities keep opening, yet occupancy rates stay near record highs in most US markets. Goldman Sachs Research expects data center demand to grow by about 50% to 92 GW by 2027. This means a yearly growth rate of 17% between 2025 and 2028. The growth rate could hit 20% if GPU power needs or customer demand rises beyond expectations. However, growth might stay around 14% if AI demand falls short.

AI leads data center growth in the United States. Power capacity should jump from about 30 GW in 2025 to 90 GW or more by 2030, growing at 22% yearly. This is a big deal as it means that the capacity needs more power than all of California uses today.

Impact of generative AI on infrastructure

The buzz around generative AI has sparked a race that needs high-density data centers and more electricity. These AI-focused facilities are a new type of infrastructure built for AI workloads. They need more absolute power, higher power density per rack, and special hardware like liquid cooling systems.

AI processing needs more power, so data centers will increase density from 162 kilowatts per square foot to 176 kW per square foot by 2027. Regular data centers are quickly becoming “AI factories” with one goal: to produce high-value tokens at unprecedented scale.

Shift from training to inference workloads

AI uses about 14% of global data center power now, but this will grow to 27% by 2027. AI workloads are changing too. AI made up about a quarter of all data center workloads in 2025, mostly from training. By 2027, inference workloads will become the main AI requirement.

AI could handle half of all workloads by 2030, with inference leading the way. This change matters because training AI models happens once or periodically, while inference creates ongoing revenue through actual use. Users need inference to work quickly, so companies must spread their facilities across regions and use embedded systems at the edge.

Big tech companies will likely control about 70% of the expected capacity in the US market. Their choices about infrastructure will shape how the entire data center ecosystem grows.

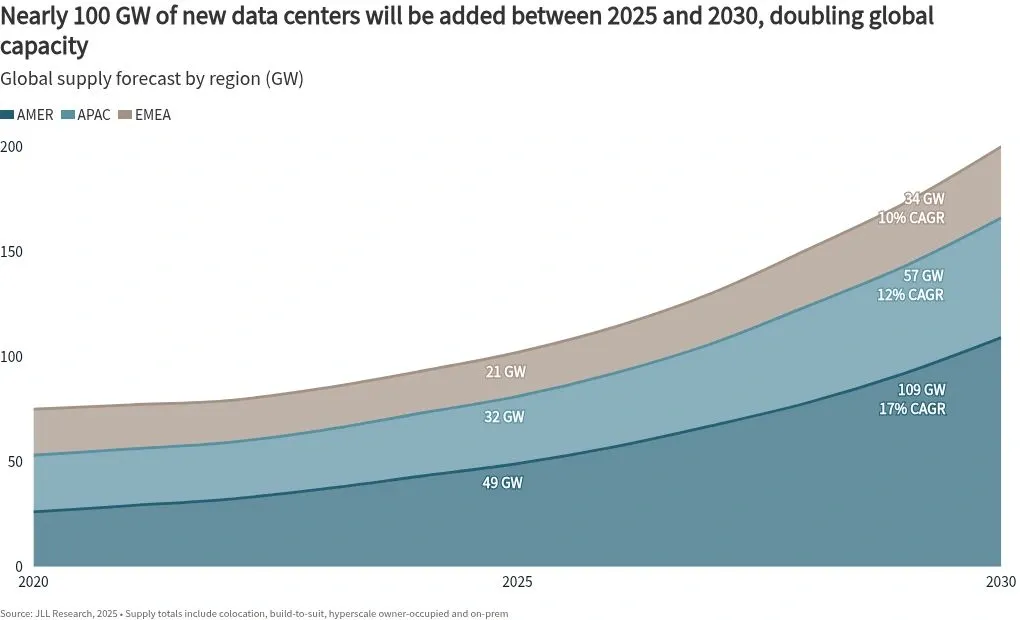

Global Data Center Capacity to Double by 2030

Image Source: Data Center Knowledge

Data center capacity worldwide stands ready for massive expansion. Global forecasts predict capacity will almost double from 103 gigawatts (GW) to 200 GW by 2030. New capacity additions will reach nearly 100 GW during this five-year period.

Forecasted capacity growth

The global data center sector shows a compound annual growth rate (CAGR) of 14% through 2030. The industry will build twice the data center capacity constructed since 2000 in less than a quarter of the time. Global occupancy rates now reach 97%, while 77% of the construction pipeline has tenants already committed. Most new capacity planned for the next two to three years has secured leases, which shows how strong the market demand remains.

Regional distribution of new capacity

The Americas will stay the largest data center region through 2030. This region represents about 50% of global capacity and grows fastest at 17% CAGR. The United States leads this growth and makes up roughly 90% of the Americas’ capacity.

Asia-Pacific (APAC) capacity will grow substantially from 32 GW to 57 GW by 2030, reaching a 12% CAGR. EMEA (Europe, the Middle East, and Africa) plans to add 13 GW of new supply with a 10% CAGR. Growth centers around established European hubs like London, Frankfurt, and Paris, along with emerging Middle Eastern markets.

Implications for hyperscalers and colocation providers

Hyperscale cloud providers own more than half of the world’s AI-ready data center capacity. These companies now build state-of-the-art facilities and team up with colocation providers to meet rising demand.

The market shows a fundamental change in development strategy. Developers prefer phased deployments of hundreds of megawatts to gigawatts. They also favor single-tenant hyperscale leases over multi-tenant colocation when possible. Hyperscalers have become more selective about long-term commitments. They apply strict criteria for power certainty, scalability, and regional risk.

Supply constraints have pushed prices up. Colocation rates in the United States rose 35% between 2020 and 2023, reversing years of steady decline.

$5.2 Trillion in AI Infrastructure Investment

Image Source: Medium

McKinsey’s research shows that AI-related data center infrastructure will need $5.2 trillion by 2030. This huge investment requirement shows how AI has altered the map of data center investments worldwide. The demand stems from the expected need of 156 gigawatts of AI-related data center capacity by 2030.

Breakdown of capital expenditure

The $5.2 trillion investment splits into three major segments. Technology developers and designers who create chips and computing hardware will receive about 60% ($3.1 trillion). The energizers who supply power generation, transmission, cooling, and electrical equipment will get 25% ($1.3 trillion). Builders will use the remaining 15% ($800 billion) for land acquisition, materials, and site development.

Investment by investor archetypes

McKinsey has identified five distinct types of investors who will drive this massive capital allocation:

-

Builders: Real estate developers, design firms, and construction companies

-

Energizers: Utilities, energy providers, and cooling/electrical equipment manufacturers

-

Technology developers and designers: Semiconductor firms and IT suppliers

-

Operators: Hyperscalers, colocation providers, and GPU-as-a-service platforms

-

AI architects: Model developers, foundation model providers, and enterprises

Hyperscalers lead this investment wave right now. Alphabet, Amazon, Microsoft, and Meta plan to invest over $350 billion in data centers in 2025 and about $400 billion in 2026.

Challenges in capital allocation

Current investment levels fall short of projected needs. CEOs hesitate to invest fully because they cannot clearly see future AI adoption patterns and face long infrastructure project timelines. Power constraints, not capital limitations, create the main bottleneck for building data centers.

This capital-intensive environment changes the AI technology landscape and might concentrate power among well-funded players. Companies now face a tough choice: they risk stranded assets by overinvesting or falling behind competitors by underinvesting.

Power Consumption to Surge 165% by 2030

Image Source: Goldman Sachs

Data centers will need much more electricity in the coming years, which will revolutionize global energy patterns. Goldman Sachs Research expects power needs from data centers to rise by 50% by 2027 and reach a staggering 165% by 2030 compared to 2023 levels.

Data center power usage projections

Data centers now use about 415 TWh globally, which makes up 1.5% of worldwide electricity consumption. This number will likely double to 945 TWh by 2030. U.S. data centers used roughly 176 TWh in 2023, which factored in 4.4% of total U.S. electricity use.

The future looks more power-hungry. U.S. data centers will increase their share from 4% to 7.8% of regional power use between 2025 and 2030, while Europe jumps from 2.7% to 5%. Some experts predict even higher numbers—data centers might use up to 580 TWh yearly in the U.S. by 2028, possibly reaching 12% of total U.S. electricity consumption.

AI’s share of power consumption

AI computing drives this massive surge. Servers optimized for AI workloads grow 30% each year, while regular servers grow only 9%. AI-optimized servers will use 21% of total data center power by 2025 and reach 44% by 2030.

AI-optimized servers will factor in 64% of new power needs for data centers by 2030. A typical AI-focused hyperscaler uses as much electricity as 100,000 homes annually. New larger facilities under construction might use 20 times more power.

Grid strain and sustainability concerns

Power grids struggle to keep up with this unprecedented growth. Data centers cluster in specific regions and strain local grids—they used about 26% of Virginia’s total electricity in 2023. Other states show similar patterns: North Dakota (15%), Nebraska (12%), Iowa (11%), and Oregon (11%).

These changes affect consumers directly. The PJM electricity market shows data centers caused a $9.30 billion price increase in the 2025-26 capacity market. This could raise monthly bills by $18.00 in western Maryland and $16.00 in Ohio. Data centers and cryptocurrency mining might push average U.S. electricity bills up by 8% by 2030.

Inference Workloads to Dominate by 2027

Image Source: MARA Holdings

AI is changing how data centers use their resources. The focus started with model training but now moves faster toward inference – where trained AI models analyze new data to make predictions.

Transition from training to inference

Several forecasts show inference workloads will become the main AI requirement by 2027. This change is happening now. Deloitte estimates inference made up half of all AI compute in 2025, and this number will grow to two-thirds in 2026. Brookfield’s projections suggest inference will take up 75% of all AI compute needs by 2030.

The business logic makes sense. Training happens once in a while as an investment, while inference brings steady revenue through actual usage. Companies now move from testing to real deployment, which means they need more AI inference servers.

Infrastructure implications

This transformation changes how companies plan and place their infrastructure. Regional hubs replace centralized clusters for inference workloads. The needs are different too – inference needs optimization and budget-friendly solutions instead of the “compute at any cost” approach that AI development used before.

Companies now look again at where to run AI workloads as their monthly AI bills reach tens of millions of dollars. AI agents that need constant inference often drive costs up the most.

Latency and edge computing needs

Speed requirements push inference toward edge environments. Cloud processing takes too long for applications that need responses in less than 10 milliseconds. Local data processing near the source cuts delays and helps make live decisions in healthcare, transportation, and manufacturing.

Edge computing brings more benefits than just speed. It reduces data transfer, protects privacy better, works during network outages, and keeps costs steady. Top organizations now use three-tier hybrid systems that combine cloud, on-premises, and edge infrastructure to get the best results.

Construction Costs Rising at 7% CAGR

Image Source: JLL

Data center projects are accelerating worldwide, but construction costs present a serious challenge. These costs are rising at an alarming 7% CAGR between 2020 and 2025. The economics of building digital infrastructure faces a fundamental transformation because of this steady increase.

Historical and projected cost trends

Data center construction costs have changed significantly in the last decade. A Tier III enterprise data center’s cost was about USD 12.00 million per megawatt in 2010. The costs dropped to USD 6.00-8.00 million per MW before COVID-19. The numbers bounced back quickly. Costs went up by USD 1.00-2.00 million per MW in 2022. The projections show USD 10.70 million per MW by 2025.

The future points to higher costs. Industry experts predict the average global cost will reach USD 11.30 million per MW in 2026, a 6% increase. Most industry professionals (60%) expect construction costs to rise by 5-15% in 2026. About 21% think inflation will go beyond 15%.

Impact on site selection and project timelines

These rising costs are changing how companies make decisions. Speed to power leads the criteria that drive site selection. Community support, latency, and customer proximity come next. Project sizes keep growing, so construction cost differences play a bigger role in choosing locations.

Lead times often stretch to 12 months or longer. This delays revenue from facilities that are almost ready. The timing matters even more since average facilities now cost between USD 500.00 million and USD 2.00 billion.

Strategies to manage inflation

Companies use several approaches to curb these financial pressures:

-

They break down projects into stages and check ROI at each step

-

They move from capital expenses to cloud-based operational expenses

-

They choose aggressive energy optimization despite higher initial costs

-

They use modular designs that allow step-by-step deployment and growth

Companies must balance their need to meet current demands with the reality of higher construction costs as they plan their long-term infrastructure.

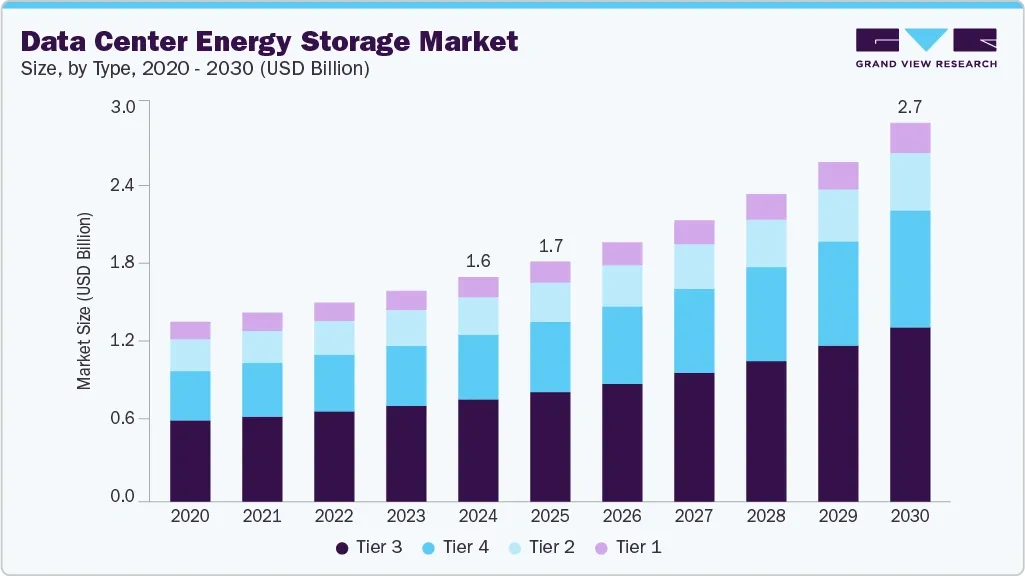

On-Site Power and Battery Storage Solutions

Image Source: Grand View Research

Data centers just need to solve their electricity challenges due to grid constraints and rising demand. A radical alteration in how these facilities ensure reliable power for critical operations is happening right now.

Behind-the-meter generation trends

The adoption of on-site power is growing faster than ever before. Data centers’ use of on-site generation will reach 38% by 2030, up from 13% last year. The numbers are even more striking when we look at facilities running entirely on on-site power. These will jump from 1% to 27% by 2030—an incredible 27-fold increase. Grid limitations cannot keep up with AI-driven demand, which explains this quick transition.

Natural gas and renewable energy roles

Natural gas is a vital component in the on-site power ecosystem. Fuel cells deliver efficiency similar to large combined-cycle gas turbines without transmission losses. These systems maintain steady efficiency whatever the load changes, which makes them perfect for handling variable AI workloads.

Natural gas works as a bridge technology that adapts to decarbonization goals. Modern gas turbines run with 30-50% hydrogen fuel content now. They aim to reach 100% hydrogen use to meet net-zero objectives.

Battery storage and grid independence

Battery Energy Storage Systems (BESS) are a great way to get more than just backup power. A single 10 MW BESS setup in a deregulated energy market could bring in $1.20-1.50 million yearly through grid services like frequency regulation.

On top of that, BESS helps save money through peak shaving, demand-response programs, and time-of-use rate arbitrage. These systems respond in milliseconds, unlike traditional diesel generators. They work as live shock absorbers that smooth out voltage fluctuations and keep power quality stable.

Data centers can recover their investment in three to five years thanks to government incentives and state-level rebates that strengthen the business case for BESS.

Cooling Innovations for High-Density Racks

Image Source: Azura Consultancy

Cooling technology plays a crucial role where data center growth meets operational efficiency. Modern facilities now use high-density racks as standard equipment, which creates new challenges for traditional cooling methods.

Liquid cooling vs air cooling

Today’s computing demands push traditional air cooling systems to their limits. These systems max out at about 25kW per rack, even with hot/cold aisle containment. Liquid cooling technologies handle much higher thermal loads up to 100kW per rack. This makes them perfect for AI workloads that need 30-40kW per rack.

The science behind this is simple. Liquids conduct heat up to 3,000 times better than air. This leads to real benefits: liquid cooling uses 10% less energy and cuts carbon emissions by the same amount. Systems that use immersion cooling can save 20% or more energy depending on their size.

Emerging technologies and vendors

The market features three main liquid cooling approaches:

-

Liquid-to-air: Coolant distribution units move heat from IT equipment to air through liquid technology cooling systems

-

Direct-to-chip: Coolant flows straight to processors through pipes, which makes it one of the quickest ways to cut energy use

-

Immersion cooling: Components sit in dielectric coolant baths that keep board temperatures lower

New breakthroughs include fiber membrane technology that pulls heat away through evaporation. Cold Underground Thermal Energy Storage (Cold UTES) creates cold energy reserves underground when demand is low.

Energy efficiency and regulatory compliance

A data center’s cooling system usually takes up 25-40% of its total electricity use. Liquid cooling technologies can cut facility power use by 27% and total site energy consumption by 15.5%.

Regulatory pressure pushes companies to adopt energy-efficient cooling solutions as we get closer to 2030. Data centers that use these technologies meet compliance rules and save money. This gives them an edge in an industry where cooling needs will double by 2030.

Server Design Evolution for AI Workloads

Image Source: JLL

As AI-driven workloads accelerate data center growth, BMS and EPMS are becoming central to reliability, efficiency, and operational control.

Avid helps data center owners and operators design, integrate, and modernize BMS and EPMS architectures that provide real-time visibility into power, cooling, and infrastructure performance — supporting high availability today and scalable growth tomorrow.

If you’re evaluating BMS or EPMS strategies for new or existing facilities, we’d welcome the conversation! https://avidsolutionsinc.com/contact-avid/